Most business owners do not run into trouble because they lack discipline or effort.

They run into trouble when the structure of their obligations no longer aligns with the reality of their cash flow.

Revenue comes in, but before it can be used to operate the business, a portion is already committed. Daily or weekly withdrawals begin to take priority over payroll, vendors, and growth. The business continues to generate income, yet it feels as though very little of it is actually available.

Over time, the pressure builds to a point where the question is no longer how to grow.

It becomes how to keep up.

For many, that is the moment where everything shifts.

It no longer feels like you are working for yourself.

It feels like you are working for the lenders first.

When that realization sets in, every business owner arrives at the same place.

What are the real options from here?

Why Refinancing Is No Longer the Reliable Exit It Once Was

For years, there was a widely held belief that if payments became too aggressive, there would always be a way to refinance into a longer term, lower payment structure.

At one time, that belief had some merit, particularly through programs associated with the U.S. Small Business Administration.

Today, that landscape has changed.

Updated lending guidelines introduced in 2025 have made it significantly more difficult for merchant cash advance obligations to be refinanced through SBA backed programs. At the same time, traditional lenders have tightened underwriting standards, placing greater emphasis on cash flow stability and existing debt exposure.

The result is a reality that many business owners are now experiencing firsthand. By the time payments begin to strain the business, the ability to refinance has often already narrowed or disappeared.

As Bob Hope once observed, a bank is a place that will lend you money if you can prove you do not need it.

While said in humor, the underlying truth resonates. Access to capital tends to be most available when it is least urgent.

Which leads to a more practical question.

If refinancing is no longer a dependable fallback, what paths are business owners actually taking?

The Five Paths Business Owners Take

When MCA obligations begin to take control of cash flow, most business owners move toward one of five directions. Each path has a different outcome, and understanding those outcomes early can make a meaningful difference.

1. Continue Paying as Agreed

This is the most straightforward option and the least disruptive when it is truly sustainable.

If the business can comfortably maintain payments while covering operating expenses and still generating profit, staying the course may be the correct decision.

The challenge is that many businesses operate under the assumption that they can manage it, when in reality they are functioning with very little margin. What appears manageable in the short term often becomes increasingly difficult as time goes on.

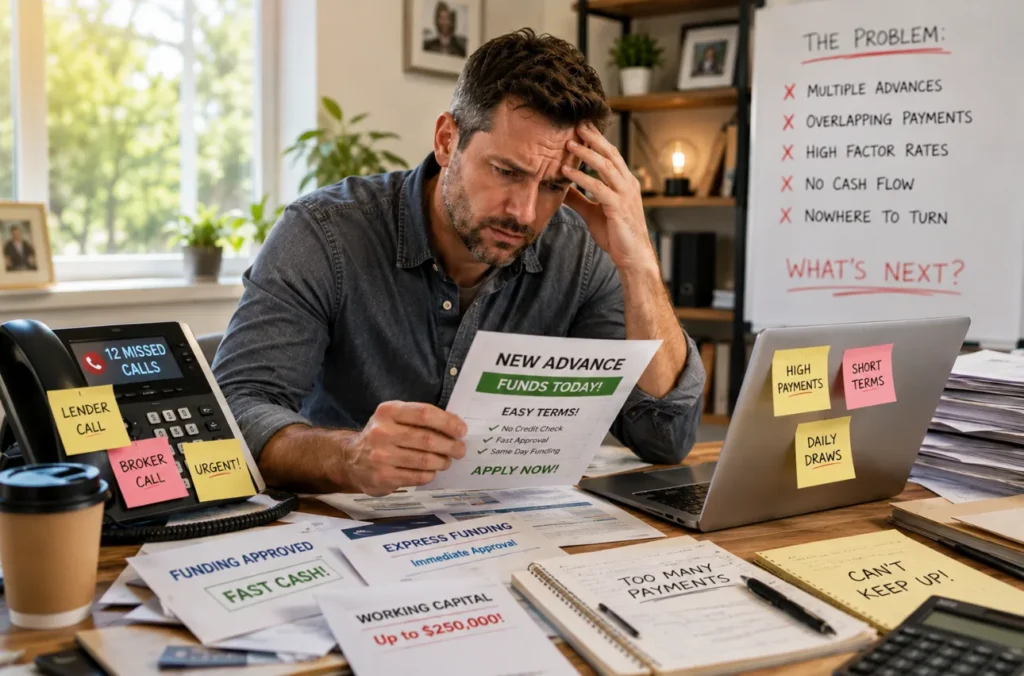

2. Add Additional Advances to Stay Current

This is one of the most common responses when pressure begins to build.

A new advance provides immediate liquidity, allowing the business to stay current and regain temporary breathing room. In the moment, it can feel like progress.

However, each additional advance increases the total obligation. Payments begin to stack, terms overlap, and cash flow tightens further.

What starts as relief often evolves into a cycle that becomes harder to exit with each step.

3. Reverse Consolidation or Reverse MCA

This path is often presented as a structured solution, yet it remains one of the least understood.

Reverse consolidation typically involves introducing new capital with the intention of managing or covering existing MCA obligations. On the surface, it appears organized and strategic. In practice, many business owners enter these arrangements without a full understanding of how the structure impacts their cash flow over time.

Rather than eliminating pressure, the structure often redistributes it.

Existing obligations remain in place while new terms are layered on top. Payments continue, and in some cases, the business finds itself managing both the original advances and the new structure simultaneously.

What makes this particularly challenging is that it often feels like progress at the beginning. There is a sense of direction and a belief that the situation is being resolved.

In reality, many business owners find themselves in a more difficult position by the time the structure fully plays out.

It is a path frequently entered with optimism and exited with frustration, largely due to a lack of clarity at the outset.

4. Traditional Debt Settlement

Another option that many business owners explore is third party debt settlement.

These programs are typically presented with the goal of reducing overall balances and creating long term savings. The process often involves pausing payments and allowing negotiations to take place over time.

While this approach can be effective in certain situations, it generally requires a period where communication with lenders is limited or delayed. During that time, business owners may experience increased uncertainty, including the possibility of escalated collection efforts or legal pressure.

For some, it provides a path forward. For others, it replaces financial strain with a different kind of stress tied to the process itself.

5. Structured Resolution Through Direct Engagement

There is another approach that focuses on addressing the situation directly rather than stepping away from it.

This method is built on a simple principle. Most lenders would prefer to recover funds over time rather than risk a complete loss if a business fails.

Firms such as Business Debt Consultants operate within this framework by initiating communication early and working to establish repayment structures that reflect the actual cash flow of the business.

Instead of avoiding the issue, the process centers on organizing it.

For business owners, this often means moving from multiple aggressive withdrawals to a more defined and manageable structure. The objective is to stabilize operations while creating a realistic path for repayment.

Those who want to better understand how these structured approaches work in practice can review additional information at Business Debt Consultants.

What Ultimately Determines the Outcome

In most cases, the difference between businesses that stabilize and those that continue to struggle is not effort.

It is timing and direction.

Waiting too long to act, relying on solutions that are no longer as accessible, or choosing short term relief that creates long term pressure can all compound the problem.

Each path leads somewhere. The key is understanding where it leads before committing to it.

A Return to Stability

When the structure changes, the experience of running the business changes with it.

Instead of multiple withdrawals, there is clarity.

Instead of constant pressure, there is direction.

Instead of reacting day to day, there is the ability to plan.

The goal is not simply to resolve debt.

The goal is to restore a position where the business can operate, stabilize, and move forward with confidence.

Written By

Financial Strategy Team at Business Debt Consultants

Focused on cash flow stabilization and structured solutions for businesses managing MCA obligations.